Over-Financialization can be our Demise

Over-Financialization can be our Demise

Post #911

“Permit me to issue and control the money of a nation, and I care not who makes its laws!” --Mayer Amschel Rothschild

When Austrian economists (free market fundamentalists) get asked about regulation, they give a unique response: cut all red tape for business but, if fiat currency holds true, then regulate-the-hell out of the banks. Austrian economists, more than anyone, understand the power a bank has if it ever gets control over the money in a nation.

This includes a central bank (an entity which, by definition, has such control).

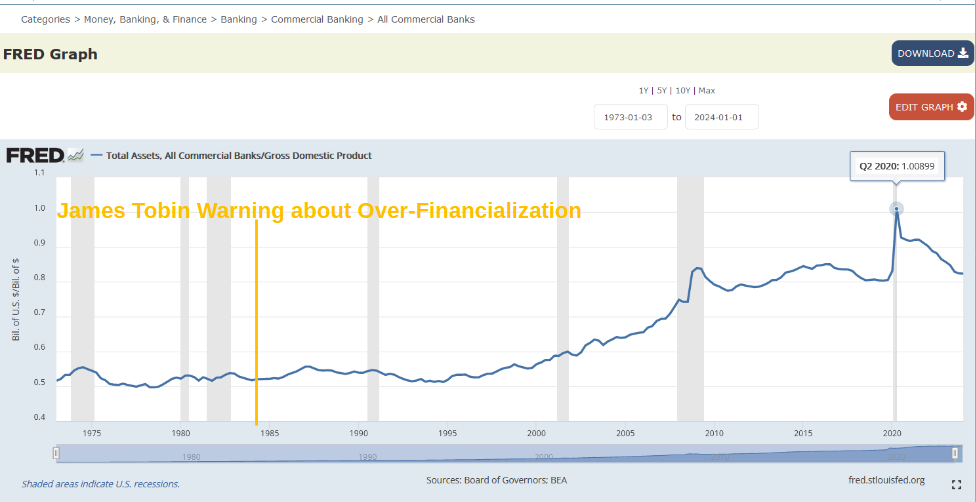

While free banking is normally good, a lethal combination is fiat currency plus free banking. Either the currency has to be brought under full control — like it is with a gold standard** — or the banks must be brought under full control. The earliest warning of over-financialization may be the one from economist James Tobin in 1984:

"... we are throwing more and more of our resources, including the cream of our youth, into financial activities remote from the production of goods and services, into activities that generate high private rewards disproportionate to their social productivity." --James Tobin (1984)

Tobin understood that you can make money by making things (which is good, because it is proof that you bettered the lives of others) but that you can also make money by making money (which is bad). Here is a graph of the size of all bank assets in relation to the size of the GDP, showing when Tobin warned us about over-financialization:

Notice how, in the second quarter of 2020, bank assets — for the first time in history — exceeded all of GDP. At left you can see what is true of healthy economies: Bank assets represent only about half of GDP, and the primary way to make money is to make things, produced things which actually do serve the wants and needs of others.

** ”full control of currency” is a phrase that was catchy but has a non-intuitive meaning here. When one party controls the currency, that is not full control of currency, it is control-by-a-minority. “Full control” means controlling the controllers — eradicating any individual control, altogether.

At Least Two Possible Ways Out

As banks progressively gain more and more ownership over all of the economy, there are two ways out of this mess: near-total control over money, or near-total control over banks. Business-as-usual (“doing nothing”) will guarantee our demise. One way to obtain near-total control over money is to return to something like a gold standard.

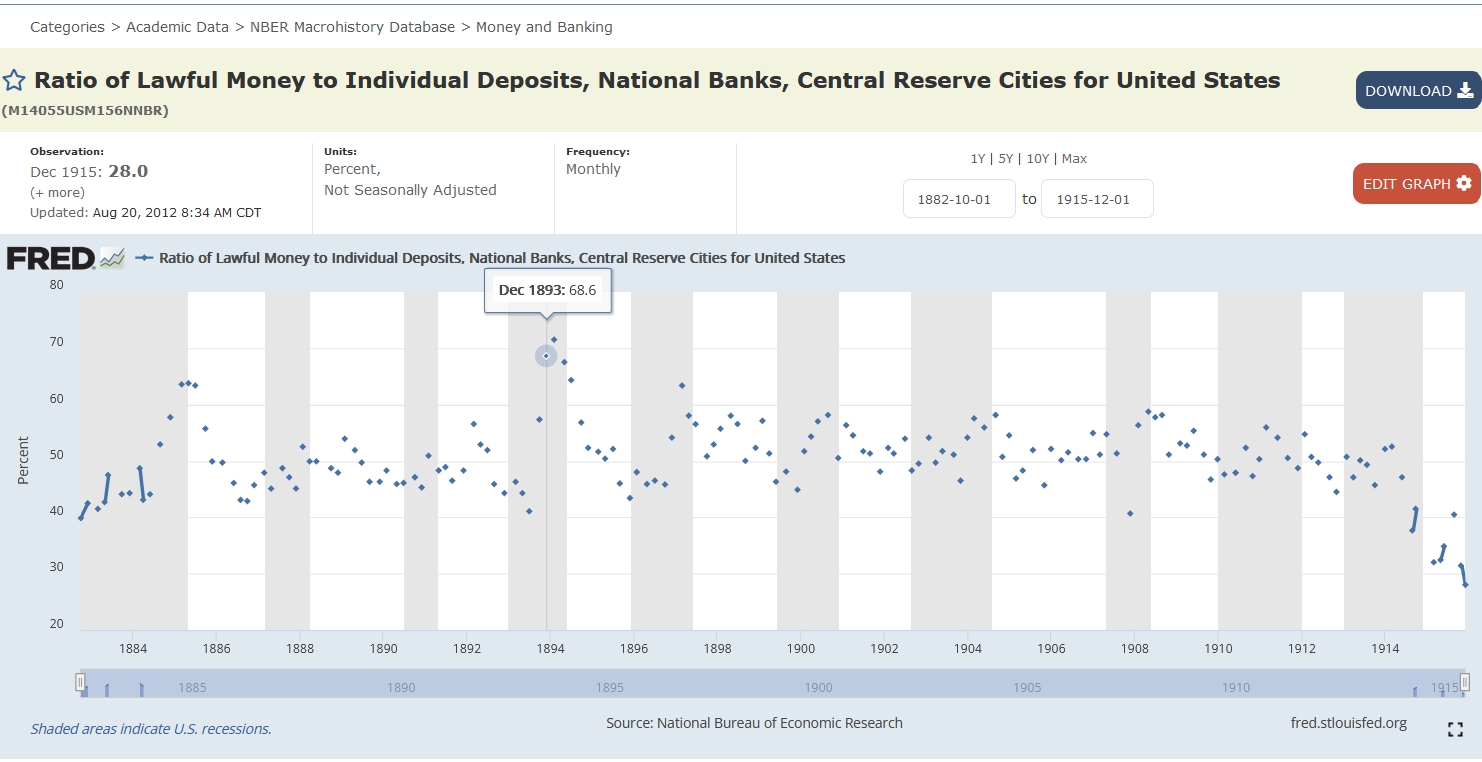

If fiat currency remains allowed, then the reserve requirements could possibly be set to at least 70% of deposits. Back in 1893 and 1894, national banks in central reserve cities were holding onto 70% reserves, and they survived it just fine (i.e., holding 70% in reserve is economically feasible for well-established banks):

[click to enlarge]

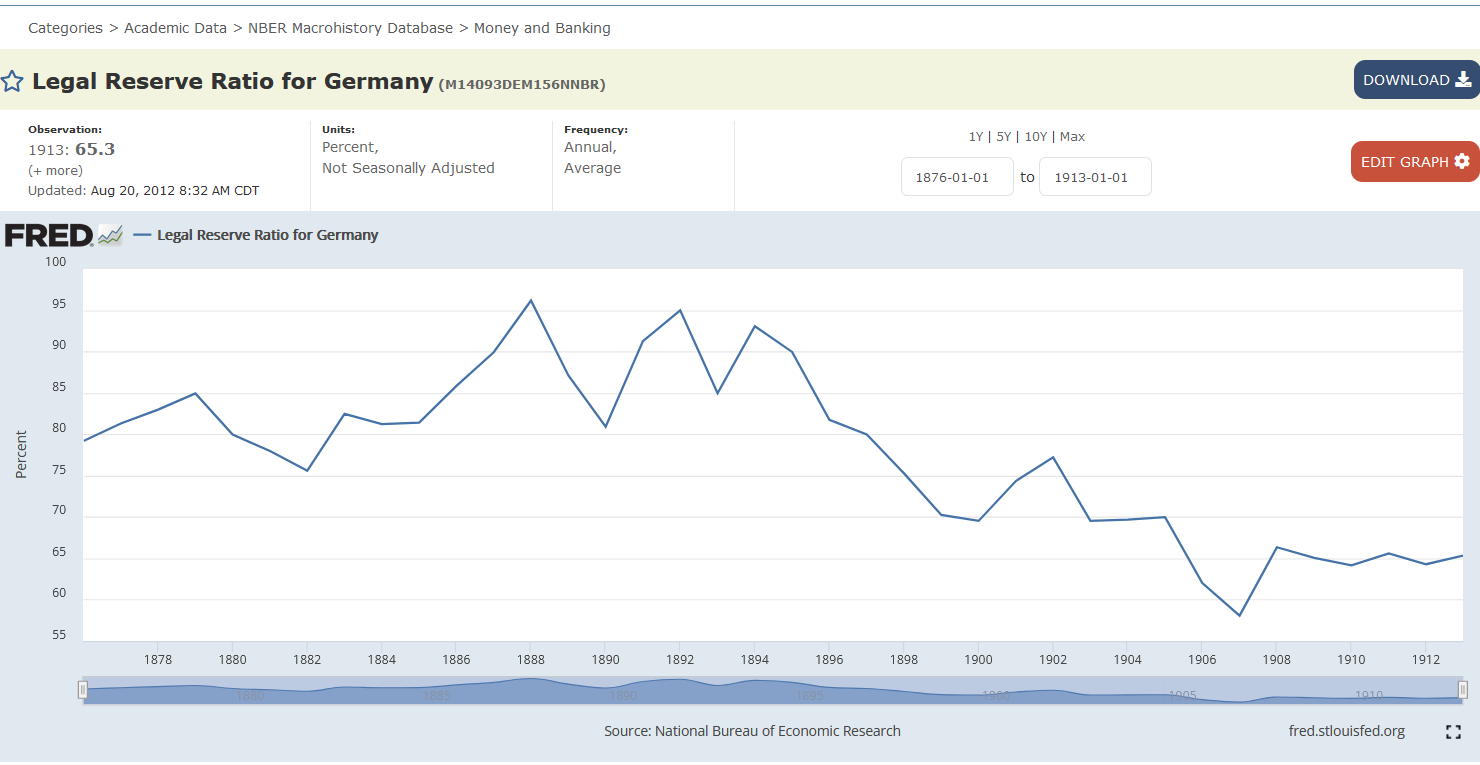

Startup banks might be allowed a sliding-scale grace period before having to hold a minimum of 70% of deposits in reserve (e.g., requirements increase by 1% a month for 70 months). Additional empirical justification for a lower bound of 70% reserves comes from the fact that it worked well in Germany for the last 23 years of the 1800s:

But here is a quote from the 2020 ruling regarding bank reserves, an action which was supposedly justified by the coming COVID crisis [emphasis added]:

Effective for the reserve maintenance period beginning March 26, 2020, the 10 percent required reserve ratio against net transaction deposits above the low reserve tranche level was reduced to 0 percent, the 3 percent required reserve ratio against net transaction deposits in the low reserve tranche was reduced to 0 percent. The action reduced required reserves by an estimated $200 billion.

The bank regulators have now showed their poker hand and have revealed that they will continue to be willing to play “fast-and-loose” with U.S. currency. But as the ‘total bank assets in relation to GDP’ graph shows, that only gives banks undue influence over resource allocation, and will ultimately lead to demise (as James Tobin predicted).

Banks make money, but they don’t make things, and that is a potential problem.

Listed Solutions Recap

Either

a return to the gold standard (or something equivalent)

or

historically-huge (70%) reserve requirements

NOTE: This post has been edited to remove the lower level of reserve requirements (35%) that it had first suggested for small or startup banks, because consistent reserve requirements as low as 35% would invite economic recessions, while reserve requirements of 70% or higher would offer more protection.

Reference

Too Much Finance? IMF Working Paper (June 2012). https://www.imf.org/external/pubs/ft/wp/2012/wp12161.pdf

I completely agree these problems very easy to solve if we had honest politicians. The only power a central bank has is the power to issue debt (print money out of thin air) and the more it can print, the more powerful it becomes. These banks are not going to give up this power and would rather kill millions of people all over the world to justify endless printing than give up any power whatsoever. We are hurtling straight for the biggest financial crises the world has ever seen and it is all carefully planned and 100% intentional. They know exactly what they are doing. They are going to make us beg for a new system and that system is digital currency they control.