Banks used to follow Good Business Practices

Post #625

Before the USA got a central bank, banks which had national charters used to follow good business practices, obviating the need for a “lender of last resort” (the need for a central bank):

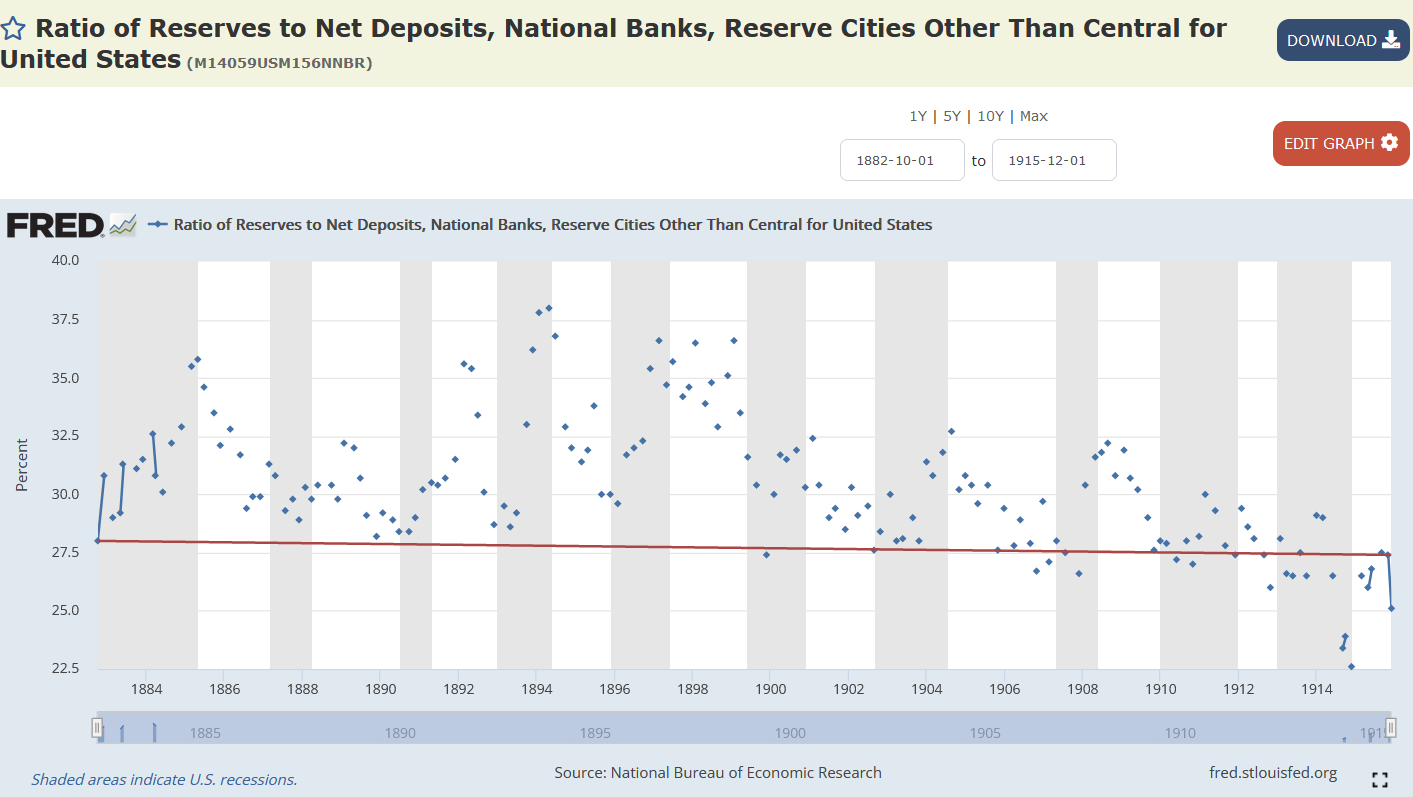

National banks in “reserve cities other than central” needed to hold 25% of deposits in reserve, just in case people wanted to take out cash. But as this graph shows, they willfully held more than that 25% in reserve (the red line is an approximate 28% reserve ratio).

But if the USA never needed a central bank, then how come we got one?

The short answer is that we were “tricked” into getting a central bank, after a couple of speculators (F.A. Heinze and C.F. Morse) tried to corner the copper market — and it was discovered that they were involved with banks and, more importantly, trusts (non-bank financial intermediaries).

However, two guys trying to corner a market in New York should not lead to an entire country getting a central bank, but it did in the USA.

After Heinze and Morse lost their lunch trying to corner the copper market, it was discovered that Morse ran 3 national banks and was on the board of directors for other ones. Even worse, it was discovered that Morse was an associate of C.T. Barney, who ran Knickerbocker Trust — the 3rd largest trust in New York City.

Bankers find a “side hustle”

Bankers had been forced by market discipline to hold high reserves, but trusts were more exempt from market forces, and they held as low as 5% in reserve, and they made risky “call loans” to stockbrokers, payable with interest in 24 hours.

Because of all of the quick cash that could be made by trusts (whose assets grew over twice as fast as banks), the bankers ended up indirectly owning trusts, through ownership in holding companies.

Bankers could not use bank funds to speculate in the stock market, but bankers could — by owning holding companies which owned trusts — benefit from that speculation. The botched speculation of Heinze and Morse brought all of this to light.

When this interlocking web of lies, deceit, and greed was exposed, people pulled out their money from the trusts (withdrew their deposits) — even though they had been such good money-makers for more than a decade.

The result is now known as The Panic of 1907, but it was just a crisis needed in order to grow support for a central bank. For the most part, banks weren’t in danger of going out of business in recessions prior to the one of 1907 — because they willfully held so much in reserve.

And they were not in danger of going out of business in the 1907 one, either. Those New York banks had nearly a 27% reserve ratio at the start of the Panic of 1907:

The lowest they got down to was 21.9% — still much higher than typical banks today. Yet that didn’t stop bankers and politicians from creating the Aldrich-Vreeland Act of 1908 and the National Monetary Commission — the precursors required for a central bank.

In the USA, we never needed a central bank to bail out banks, per se, but we got a central bank to bail out the interlocking web of lies, deceit, and greed practiced by certain individuals working inside of banking. Bad actors making good people pay.

The 2008 financial crisis was merely a repeat of the exact same thing as in 1907:

Bankers finding a “side hustle” — but this time in mortgage-backed securities, derivatives, and collateralized debt obligations.

And just like before, we lost our assets based on their bad behavior, because they were able to rig the system in 1913.

Reference

National Bureau of Economic Research, Ratio of Reserves to Net Deposits, National Banks, Reserve Cities Other Than Central for United States [M14059USM156NNBR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/M14059USM156NNBR

National Bureau of Economic Research, Ratio of Reserves to Net Deposits, National Banks for New York, NY [M14061US35620M156NNBR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/M14061US35620M156NNBR

[National banks needed 15% to 25% in reserves, but typically held even more] — https://www.federalreserve.gov/pubs/feds/2013/201311/index.html

[1907 was the impetus/excuse given for a central bank] — https://www.minneapolisfed.org/about-us/our-history/history-of-central-banking

[National banks had indirect exposure to failures in the New York City trusts through the “firesale effect” of them calling-in all of their call loans (i.e., the sold stocks shares would increase stock share supply and drop the stock prices by so much that bank assets fall with them)] — https://www.federalreservehistory.org/essays/panic-of-1907