Makers of Money vs. Makers of Things

Makers of Money vs. Makers of Things

Post #468

... we are throwing more and more of our resources, including the cream of our youth, into financial activities remote from the production of goods and services, into activities that generate high private rewards disproportionate to their social productivity.

James Tobin (1984)

Notice how this quote can be interpreted as dividing the world into people “who make money” (banking & financial services) and people “who make things” (rest of the economy). Over-financialization is thought to make economies less resilient.

With the recent bru-ha-ha reported on by Dr.

regarding biometric-validated digital banking IDs — which opens the floodgates for central bank digital currencies (CBDCs) — it pays to wonder if those who deal only in money (ie., the financial system) are disconnected from those who make and sell things (everyone else).It pays to wonder:

If they get control of your money, then will they have control of your life? Typical street thugs usually give you an option: “Your money or your life!” But those in charge of the world’s financing could conceivably have control over both.

That’d make them even worse than street thugs (street thugs leave you alone after they’ve taken your money away from you). But CBDCs, if allowed, will let strangers have disposal over your very life.

Banksters

It’s normal for banks to hold cash in reserve in case you’d like to draw your money out. In the early 1900s, national banks held between 25% and 30% of deposits in reserve (green markings added):

But banks make more profit if they lend out more money, so it’d be in their special interest to hold less in reserve (lending more out), or no reserves at all — lending it all out. By 1992, banks got a sweetheart deal:

Not only did they no longer need to hold anything in reserve on savings accounts (right side, bottom), but they only had to hold 10% in reserve on the money deposited into checking accounts (left side, bottom).

Banks had a field day with their new lending capacity. The people “who make money” were doing better off each year, while the people “who make things” (the nonfinancial sectors of the economy) were starting to be left behind, mostly due to debt accrual.

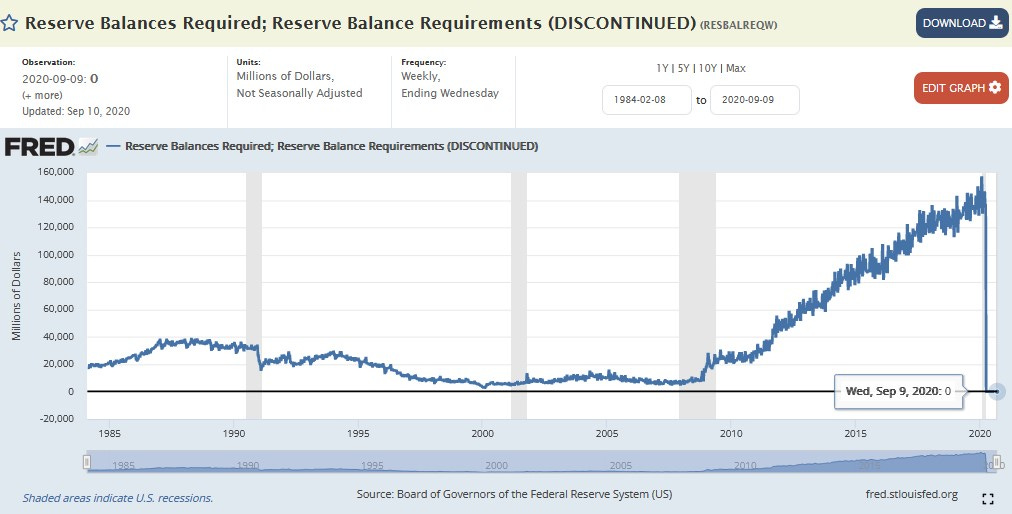

By 2020, those “who make money” had decided to give themselves even more leeway to profiteer:

0% reserve requirement

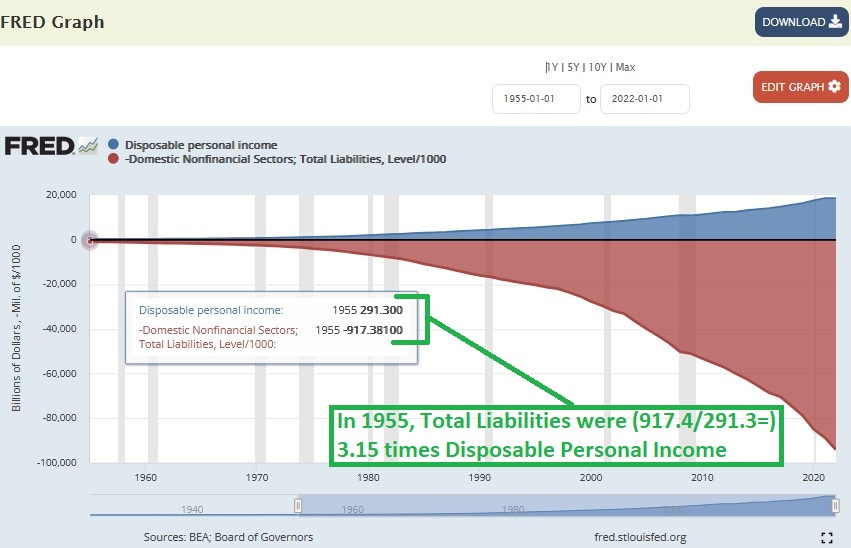

Let’s evaluate the result of all of this “bankstering” by documenting the progression of the debt-to-disposable income ratio over time (blue=income; red=debt; green markings added):

Back in 1955, the people “who make things” did very well, and the total liabilities in all non-financial (non-bank) sectors was only 3.15 times the disposable income.

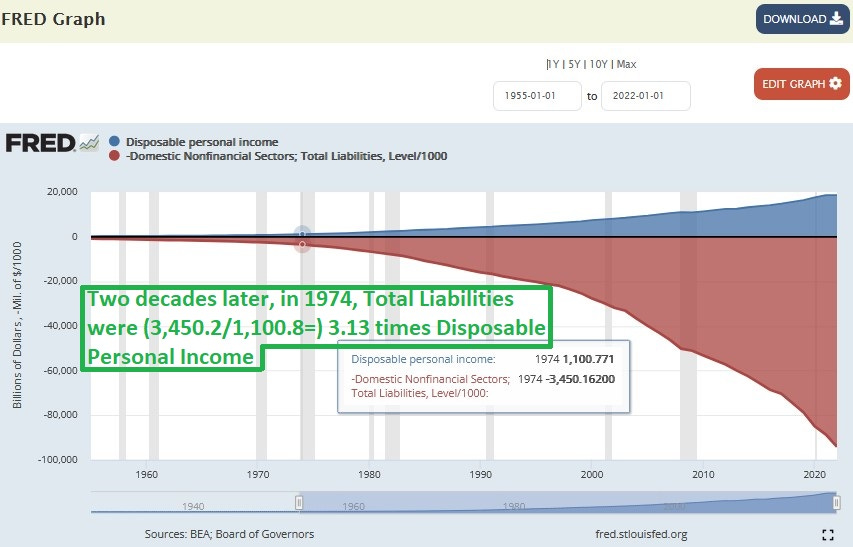

By 1974, things were still going well for the middle-class and the working-class in America, and the total liabilities were 3.13 times the disposable income. But the US had just went all of the way off of the gold standard, allowing those “who make money” to get rich quick.

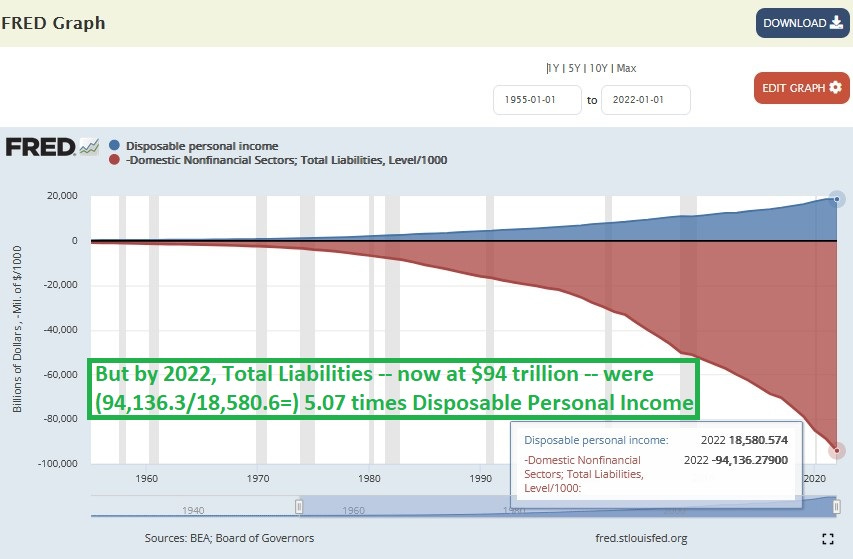

Let’s check into the situation of 2022 now:

Total liabilities in 2022 reached $94 trillion and were over 5 times the disposable income.

The increasing steepness in the red line indicates that this situation is expected to grow worse, with every year that passes. That’s because you cannot support an economy by simply “trading money.” You have to have an economy that works for those people “who make things.”

Here are 4 things required to ensure that the economy works for everyone:

low government spending

low government regulation

sound money

free trade

As the increasingly-steep red line shows, the only other alternative to restoring economic freedom in the USA is to slide into dictatorship, along with the squalor it brings, where those in government have full control over spending.

That type of dictatorship is exactly what CBDCs will bring about.

Reference

[source for quote at top and also for concern over hyper-financialization] — Too Much Finance? Jean-Louis Arcand, Enrico Berkes and Ugo Panizza. https://www.imf.org/external/pubs/ft/wp/2012/wp12161.pdf

I'm the last person to ever defend derivatives and securitization, but occupational obsolescence is an irresistible incentive toward accrual of passive income, even among those who would otherwise abjure the temptation to become predators and parasites.

I don't think any discussion of financialization is coherent without factoring in the accelerated rate of change that is the hallmark of this era.

Entropic effects on monetary supply and velocity are readily understandable in an economy based on commodity production and conversion, but offshoring and unfettered international capital migration have allowed self-interested Keynesians to hold far too much control over the public's conceptualization of these matters and their sleight-of-hand has been very successful in keeping the toiling classes quiescent.