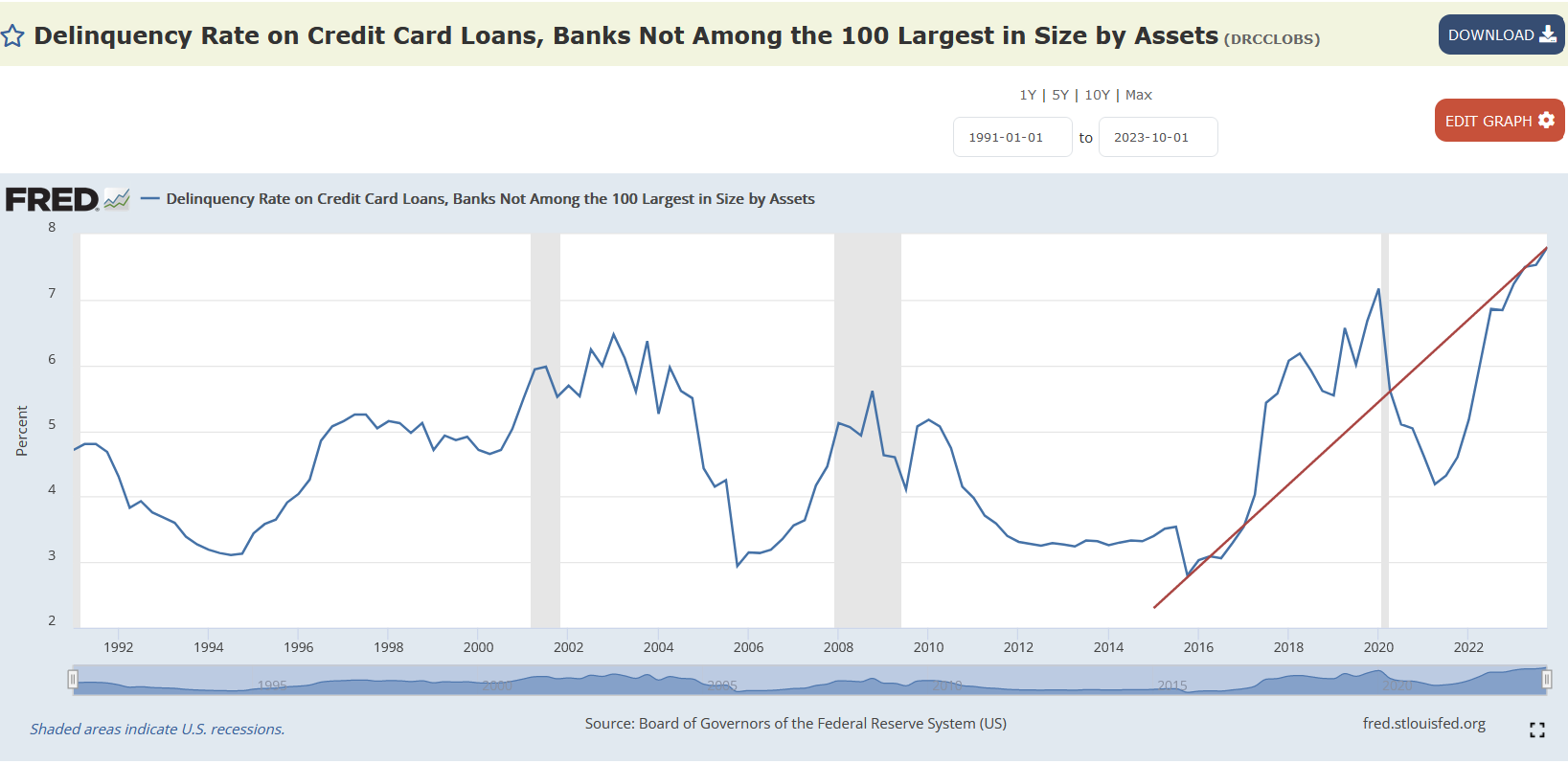

Small-Bank Credit Card Delinquency Rate

Small-Bank Credit Card Delinquency Rate

Post #765

For the past 8 years, the proportion of all credit cards issued by small banks that are delinquent has been growing:

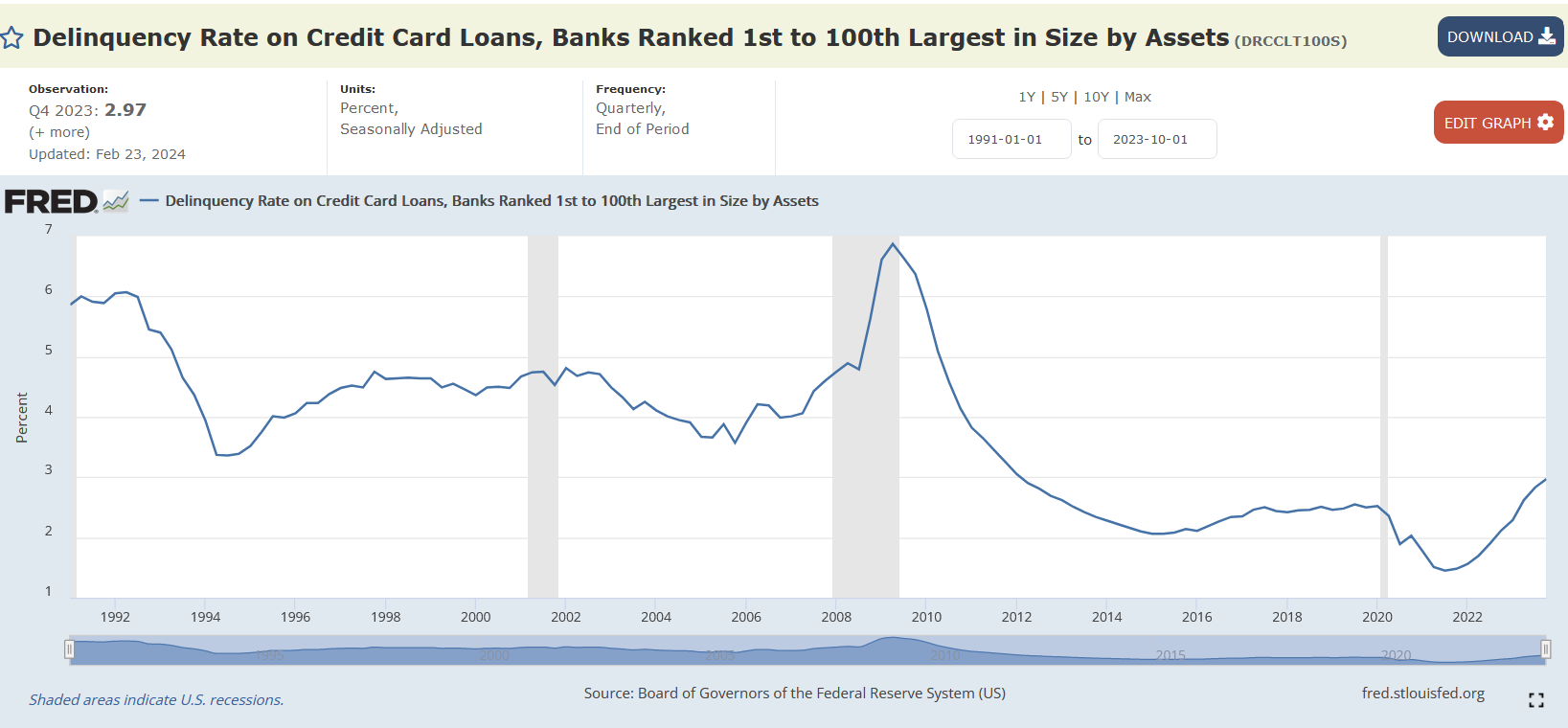

These small banks may be an early-warning indicator, like a canary in the coal mine, due to being susceptible to financial stress. The same trend exists, but is not anywhere near as bad, with the top 100 banks:

The New York Fed reported on how over 6% of issued credit cards transitioned into serious (90-day or more) delinquency in Q4 2023. The annualized rate, but applied to the outstanding balances not the number of issued cards, was over 8% transitioning into serious delinquency.

The small-bank credit card delinquency rate more-closely tracks such changes.

The evidence suggests that we need to downsize the federal government and free up the markets, because the government is, once again, leading us into an economic tar pit.

Reference

Federal Reserve Bank of New York. Credit Card and Auto Loan Delinquencies Continue Rising; Notably Among Younger Borrowers. February 06, 2024. https://www.newyorkfed.org/newsevents/news/research/2024/20240206