When people go to apply for a home mortgage, the lender looks at metrics to determine if there is a high chance of default. One metric is the debt-to-income (DTI) ratio where debt servicing costs are compared to income.

If all of your bills amount to $1,050 a month, but your income is $5,000 a month, then your DTI is 21% — and you are likely to get approved for your mortgage. Here are the mortgage lending standards which prevailed before our recent history:

Good: Debt service costs are 30% of income or less

Acceptable: Debt service costs are over 30%, but still below 36%

Bad: Debt service costs are over 36%, but still below 43%

Unacceptable: Debt service costs are over 43% of your income

Even if the average interest on all debt owed by all nonfinancial (non-bank) sectors was 9%, the USA would have still only had ‘interest-only’ payments that were 21% of income — if you are looking just at the year of 1948. We had “good credit” back then, because the sum total of all liabilities was less than 3 multiples of income.

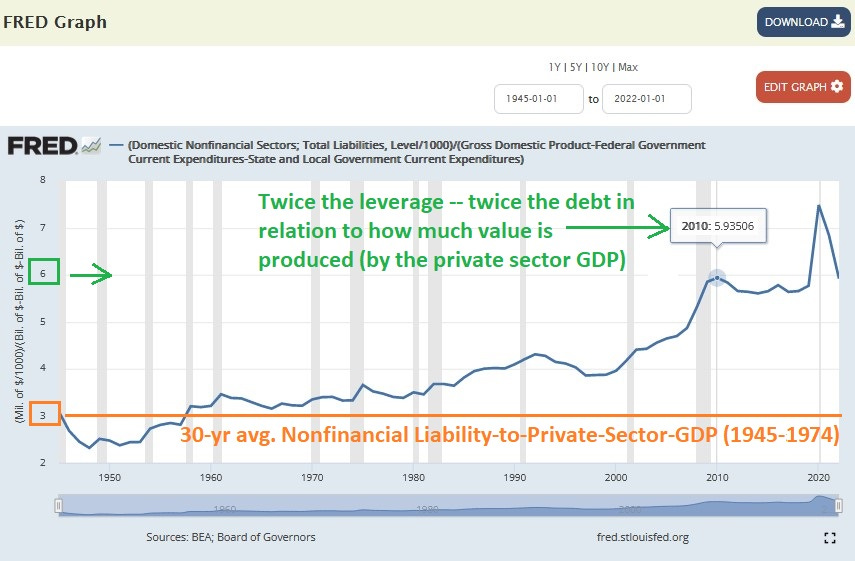

Here is the ratio of all liabilities to the income/expenditure of the private sector over time:

[click to enlarge]

The first 30 years of data, from 1945 to 1974 inclusive, reveal an average of 3.0 — where the total liabilities were 3 times the private sector income. Here is a noted graph showing that:

[click to enlarge]

But notice the current millenium (post-2000), when a protectionist corporate fascism surged in America, and the number of “public-private partnerships” ballooned. The extra government intervention into the economy resulted in a steep rise in debt-to-income.

The 3 main parts of nonfinancial liabilities are households, businesses, and government. At the debt load we now face (thanks to government interventions), if the average interest rate across all sectors were to hit 7%, then most lenders would turn us away rather than granting us a hypothetical mortgage.

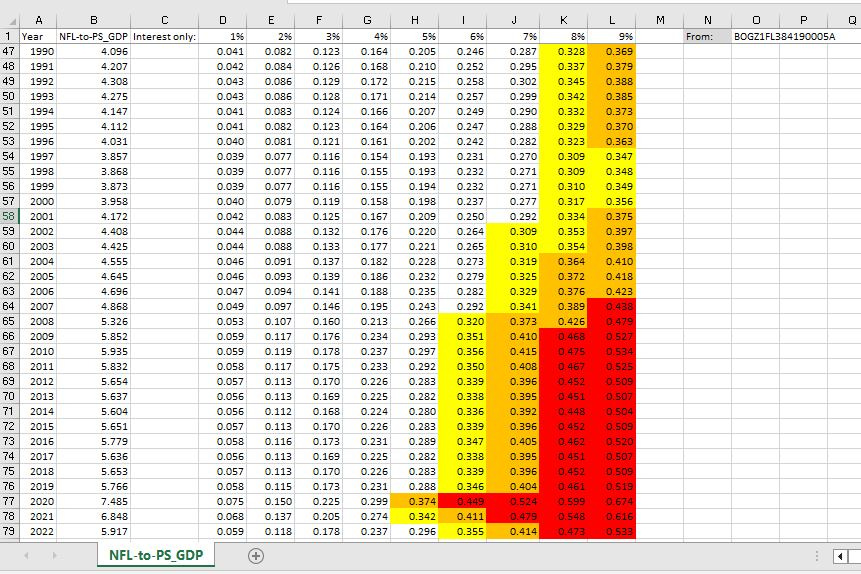

And that’s just looking at paying “interest-only” payments which don’t even touch the principal of what is owed. Here is a table showing the fraction of domestic income taken up by “interest-only”:

[click to enlarge]

Debt became so high in relation to income by 2007 that, if the average interest on all debt hit 9%, our nation would be “red-lined.” By 2009, debt was so high that even an average of 8% interest would make lenders turn us away.

In 2022, things get scary when the average interest paid on debt hits 6%, and 8% is a “deal-breaker.” This is important because the average interest rate paid by all sectors combined has a floor, for the most part, at the federal funds rate (overnight lending to banks) — which just went past 5% recently:

[click to enlarge]

Evidence suggests that “public-private partnerships” which are inherently not primarily profit-driven (because the personal initiatives of government officials carry too much weight) need to be dismantled. Intervention in general needs to wither away, returning us to the self-sustaining prosperity only found with free enterprise.